Peter Costello’s 2006 simplified superannuation rules seem a lifetime ago. In complete contrast the 2016 Federal Budget contains complexity, retrospective rule changes and personal and company tax[...]

“Still today, the definition of investment risk remains the volatility of share prices…we refuse to accept volatility as a problem. Our primary risk is not losing money but outliving it.” –[...]

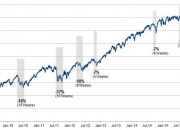

In light of the recent market pullback we have provided the following charts to provide perspective of the longer term which paints a much different picture: The first chart below shows the return of [...]

With government finances continuing to decline and our federal treasurer suggesting working Australians should forget about relying on the aged pension we thought the following riddle might make for g[...]

In building an investment strategy to provide independent income streams for life after work we continue to analyse different asset returns given the impact of inflation is often underestimated. Eve[...]

To ensure clients continue to get optimal investment outcomes we are continually seeking out reliable research and in the last few weeks the 30 June 2015 SPIVA Scorecard was released. This is a regu[...]

At the height of the GFC in 2008, a $500,000 lump sum was enough to generate income equal to the aged pension. Today with interest rates plummeting to generational lows the lump sum has blown out to[...]

In late May 2015 the banking regulator (APRA) has tackled the banks in an attempt to curb a rapid expansion in investor lending (and rapidly increasing property prices mainly in NSW and VIC) given 50+[...]

With the possibility of a new superannuation tax flagged by the Federal Opposition Leader of 15% tax on income over $75,000 pa within a super fund – Q: Does it still make sense to contribute to supe[...]

Every 5 years the Australian government commissions an Intergenerational report to assess the sustainability of economic policy setting based on projected population trends and other demographics. [...]